The Insurance Regulatory and Development Authority of India (IRDAI) expects India to become the sixth-largest insurance market in the world by 2034, overtaking South Korea, Italy, Canada and Germany. India’s life insurance sector is growing at a CAGR of 32%-34%, driven largely by rising incomes and awareness regarding insurance coverage benefits. As a result, the overall insurance sector in India is expected to be worth $222 billion by 2026.

However, this exponential growth has given rise to fierce competition, with insurers racing to offer the latest innovations in the industry. Against this backdrop, the best way to stay ahead of the curve and capture a larger market share is by staying updated on the latest trends in the sector. Interestingly, a large percentage of these trends are being driven by advances in InsurTech, which are increasing the reach and efficiency of insurance companies in India. So, here’s a look at the innovations that will redefine insurance over the coming years.

Customer-Centricity

Customer-Centricity

Customer experience is the secret ingredient to customer acquisition, retention and loyalty. Gaining customers isn’t enough. Insurers need loyalty for repeat purchases. Advanced technologies that ease the customer’s journey and provide support throughout their lifecycle with the insurance company are, therefore, gaining popularity. Technological advancements are also playing a central role in streamlining operations to provide smooth and hassle-free customer experiences.

One of the biggest elements in elevating customer experiences is personalisation. Tailored policy recommendations, pricing and support services are being eased through AI and data analytics. While AI-powered virtual assistants are redefining customer interactions, data analysis provides insights into opportunities to cross-sell and upsell.

Another customer-centric transformation is the prioritisation of digital solutions. The insurance sector in India is becoming increasingly aware of the digital-first inclination of today’s customers. Millennials and Gen Z prefer to interact with brands via digital channels, access products and services on mobile apps, and apply for insurance and file claims online. The digital-first approach is also benefiting insurers by providing access to big data, which can be leveraged to make strategic business decisions.

Shift to Self-Service Facilities

A recent survey has revealed that 81% of customers, including insurance policyholders, want self-service facilities. The modern consumer wants greater autonomy. They feel more in control when they can resolve issues without needing to reach out to customer support over the phone or email. This DIY approach extends to making policy purchase decisions, managing their policies, checking premium payments, filing claims and more. So, providing self-servicing can lead to higher customer satisfaction.

Self-service facilities can also be advantageous for insurance providers. They can enhance employee productivity, lower customer acquisition costs, accelerate claims processing, build brand value and increase customer retention. So, what features should a self-service platform possess in the insurance industry? Here’s a look.

Intuitive interface: User-friendly navigation and easily accessible platform on a variety of devices.

Personalisation: Customisable dashboard for the customer to allow convenient policy management.

Feature-rich: Multiple functionalities, such as easy payment processing, electronic signatures and access to knowledge resources.

Offering such a self-service platform can position a brand as one that is committed to meeting evolving customer needs while ensuring utmost convenience. Such a brand image can work wonders in attracting and retaining customers, given that consumers today are quick to switch insurance providers if they find a more user-friendly platform.

Powering Digital Transformation with AI

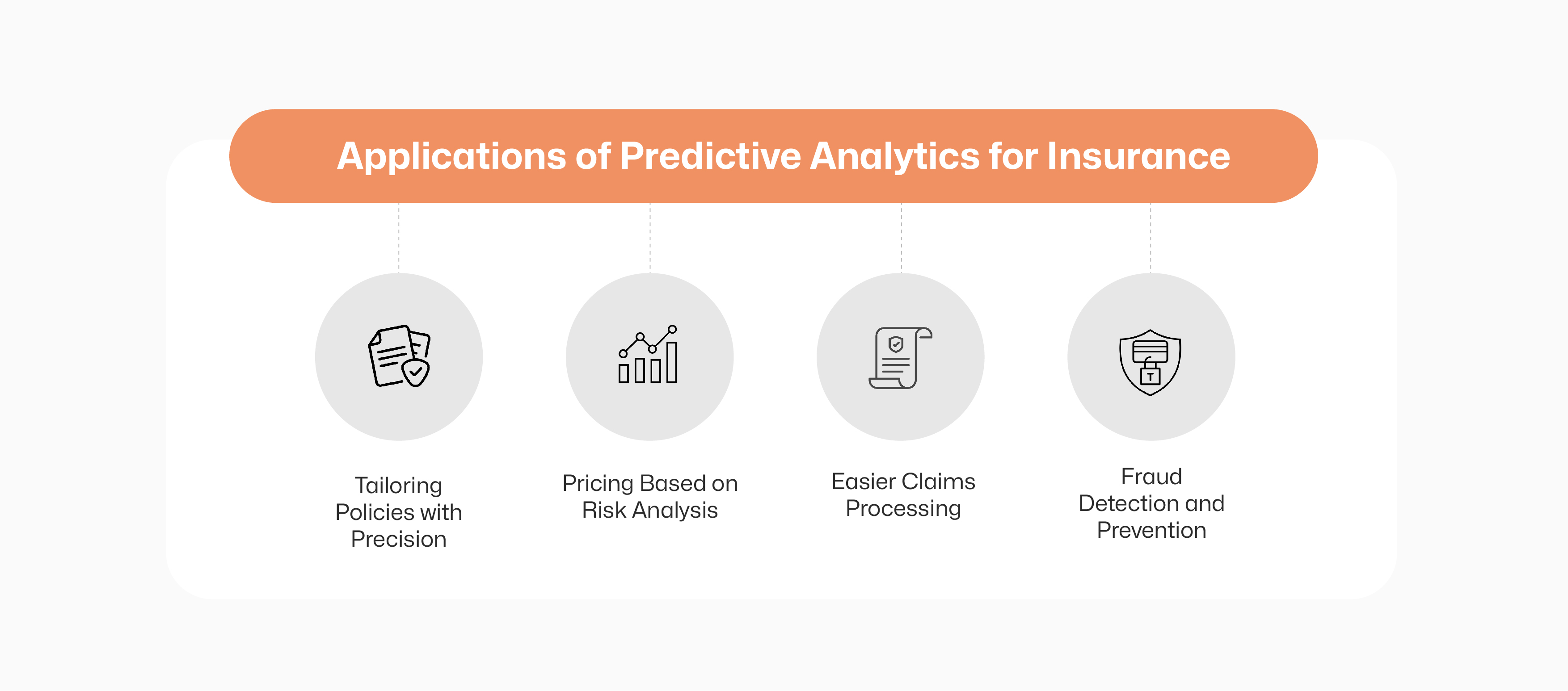

AI/ML are no longer mere buzzwords. They are being widely used for risk assessment, fraud prevention, personalisation of policy recommendations and much more. In fact, AI/ML is driving business success by automating routine tasks, increasing operational efficiency and enhancing productivity. But perhaps the area in which this technology is proving the most beneficial, not just for insurance but also for InsurTech companies in India, is predictive analytics.

By analysing massive datasets, AI/ML helps insurers identify market trends, customer behaviour patterns, risks and more. With these insights, not only can policies be tailored to fit customers, based on their behaviour patterns, but pricing can also be determined to provide the best-fit premium based on risk analysis. By addressing customer needs even before they arise, insurance companies can position themselves as brands that understand their target market. This helps build credibility and trust.

Predictive analytics can also be a game-changer in identifying policyholders who are likely to cancel their policy or move to lower coverage. With such insights, insurance companies can reach out to these customers and provide personalised attention to resolve issues and raise satisfaction levels. Early warning signs can help brands move proactively to retain clients.

Predictive analytics can also be a game-changer in identifying policyholders who are likely to cancel their policy or move to lower coverage. With such insights, insurance companies can reach out to these customers and provide personalised attention to resolve issues and raise satisfaction levels. Early warning signs can help brands move proactively to retain clients.

Another area where predictive analytics can be immensely useful is identifying potential target markets. Insurance uptake is penetrating deeper into India, with people in Tier 2 and 3 cities increasingly buying policies. In fact, analytic insights can also inform marketing strategies in different markets to ensure maximum impact. InsurTech companies in India are constantly innovating to help insurers capitalise on the power of predictive analytics.

E-underwriting and Claims Processing

The time and effort required to underwrite policies can be significantly reduced with technology solutions for underwriting. Evaluating risks and pricing policies can be automated, eliminating human error and delays. Similarly, processing claims can be expedited through digital transformation, with AI-powered automation assessing claims in a fraction of the time taken by manual processes. This reduces wait times for customers, enhancing their satisfaction with the insurance provider.

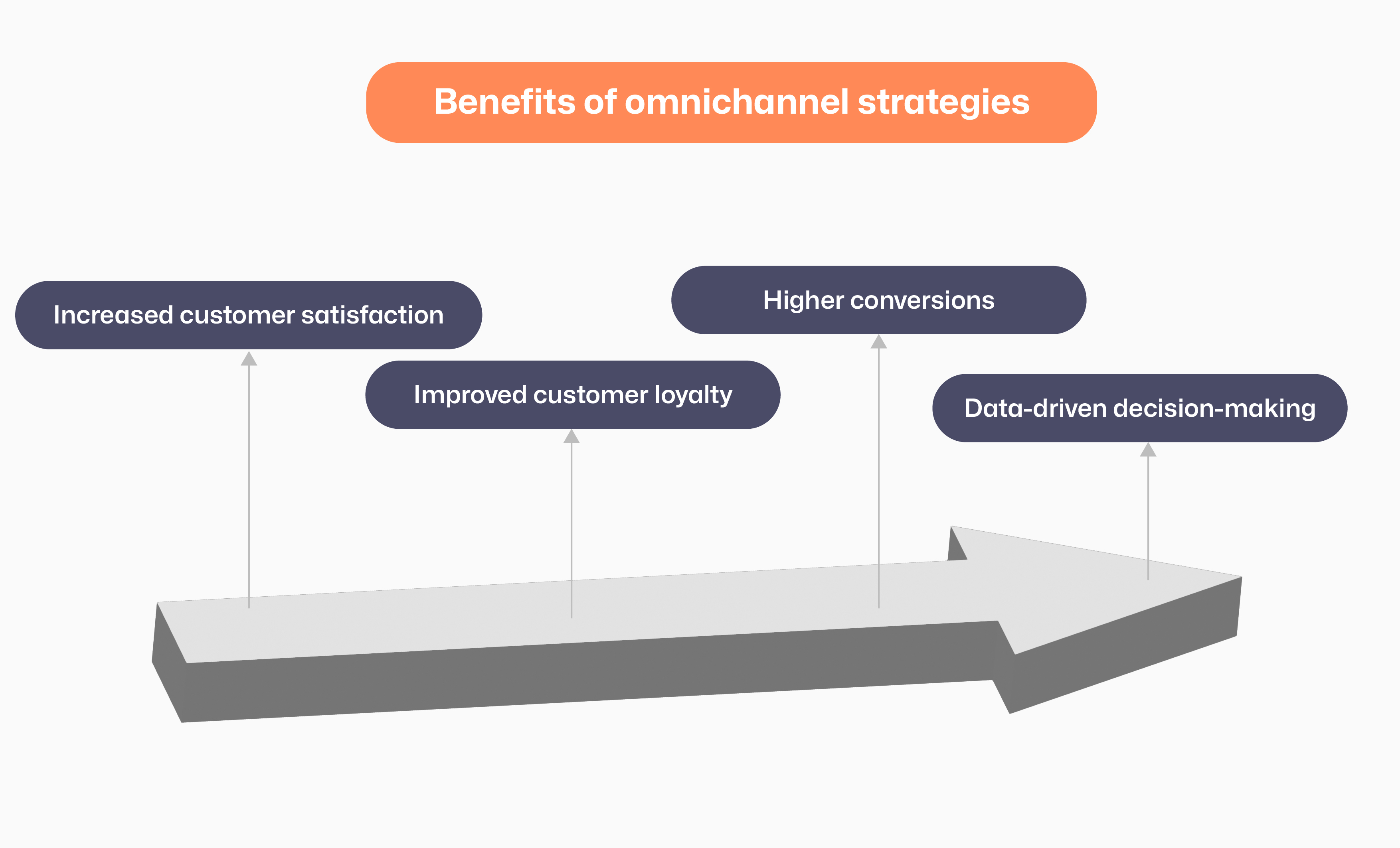

Omnichannel Customer Interactions

From traditional face-to-face interactions and phone calls, insurance is rapidly adapting to the changing customer expectations of being able to reach out to insurers anytime, anywhere. In the digital era, the consumer researches policies online, checks out reviews on social media, and seeks information via live chat on insurance websites and support on the mobile app. Therefore, an omnichannel presence is fast becoming a necessity rather than a luxury.

However, omnichannel customer experiences need careful planning. They need to be consistent across digital and offline touchpoints. Plus, the customer's information should be accessible on-demand if they ever visit a physical branch for assistance. The key to a successful omnichannel strategy is to provide seamless experiences across channels and throughout the customer journey.

Embedded Insurance

Embedded Insurance

Just like embedded finance is gaining ground worldwide, embedded insurance is also making inroads, driven by collaborations between traditional insurers and InsurTech companies in India and other countries. This allows insurance providers such as car dealerships or electronics retailers to offer coverage at the point of sale. This innovation is expected to bring significant opportunities worth about $900 billion by 2040.

With embedded insurance, the industry will see a major transition from traditional, rigid models to usage-based, dynamic policies that adapt to individual needs. The result will be the availability of protection seamlessly integrated with everyday activities. Embedded insurance will be supported by advancements in AI/ML, cloud computing, APIs, blockchain, and other technologies. These technological advancements will support scalability, smooth data exchange in real-time, personalisation of services, stronger security and effortless claims processing.

A New Era of Collaboration

The insurance sector in India is poised for significant growth, unlocked through strategic partnerships with InsurTech companies. Such collaboration brings together the wide experience of established players and the flexibility and scalability of technology to offer customers just-in-time, on-demand products and services. In fact, statistics reveal that such collaboration can lead to a 90% reduction in fraud performance, driven by proactive technology-powered intervention. InsurTech powers insurers with a data-rich, digital ecosystem that promotes innovation to deliver new value propositions to end users.

Strategic partnerships offer a meaningful advantage, allowing traditional insurers to compete with new, disruptive entrants in the industry. The brave new world of insurance is poised to witness explosive growth, supported by technology that drives accessibility and financial inclusion.

Bibliography

https://www.ibef.org/industry/insurance-sector-india (last accessed on August 2, 2024)

https://get.nice.com/Digital-CX-Research-Report.html (last accessed on August 2, 2024)

https://www.cnbctv18.com/finance/india-second-largest-insurance-technology-market-in-asia-pacific-report-9341191.htm (last accessed on August 2, 2024)

https://bfsi.economictimes.indiatimes.com/blog/insurance-trends-that-will-reshape-indias-financial-landscape-in-2024/106255001 (last accessed on August 2, 2024)

https://www.pwc.com/gx/en/financial-services/fs-2025/pwc-insurance2025.pdf (last accessed on August 2, 2024)

https://www.magnolia-cms.com/blog/the-power-of-omnichannel-experience-in-the-insurance-industry.html (last accessed on August 2, 2024)

https://www.mckinsey.com/industries/financial-services/our-insights/insurance-blog/itc-dia-europe-2023-five-insights-on-the-future-of-insurtech (last accessed on August 2, 2024)